By CRM Staff

Victoria, British Columbia — July 26, 2017 — The rates currently charged by the Insurance Corporation of British Columbia (ICBC) for basic auto insurance are not sufficient to cover the cost of automotive and personal injury claims, according to a new report by Ernst & Young.

“Over the past several years, the Insurance Corporation of British Columbia (ICBC) has experienced rapidly increasing vehicle repair and bodily injury claims costs, as well as a concerning increase in the number of car crashes on BC roads. This represents a significant change from the steadily declining accident rates and relatively stable premiums that had occurred over the previous decades,” according to the authors of the Ernst & Young report, “Affordable and effective auto insurance – A new road forward for British Columbia.”

Any vehicle registered for driving in British Columbia must, by law, be covered by ICBC’s Basic insurance package, Basic Autoplan. Basic Autoplan includes protection from third-party legal liability, under-insured motorist protection, accident benefits, hit-and-run protection and inverse liability. BC drivers also have the ability to buy optional insurance for additional coverage such as extended liability, collision and comprehensive plans. Optional insurance can be purchased from ICBC or from private insurance firms.

The report notes that the auto insurance landscape has evolved greatly across Canada, with a mixture of public and private providers as well as different insurance models in place. BC has a litigation-based insurance model, which allows not-at-fault drivers to sue at-fault drivers for both economic loss and pain and suffering, regardless of severity of injury. BC is the only province in the country that has not modified this model.

In brief, the issues impacting ICBC are that the premiums are the second highest in Canada), yet are not high enough to cover the true cost of paying claims. More accidents are occurring on BC’s roads, and the number and average settlement of claims are increasing. Government intervention has protected BC drivers from the currently required 15 to 20 percent price increases, but the situation is not financially sustainable.

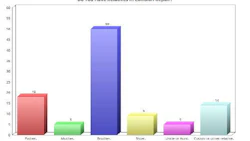

Minor injuries account for about 20 percent of the total annual cost, while serious and catastrophic injuries account for less at just 17 percent. According to the report, minor soft-tissue injury costs are only about half of more serious or catastrophic injuries in most other jurisdictions.

The litigation-based model currently used by ICBC also has significant legal costs. According to the report, legal costs account for 24 percent of total annual costs. This alone is greater than the cost to run ICBC and the benefits received by either minor injuries or non-minor injuries.

“In summary, the BC auto insurance system has significant structural problems. However, based on the experience of other jurisdictions, there are proven solutions available, but this additional work needs to start now,” according to the Ernst & Young report.